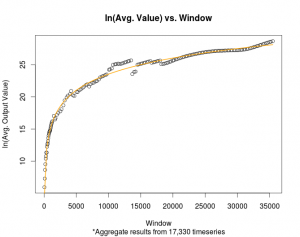

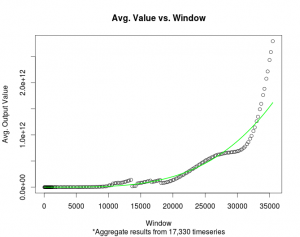

There are now 17,330 individual time series monitored by The Bubble Index; each with a full range of windows. The windows range from 52 to 35,500 days. Below is plotted the natural log of the mean value (y-axis) versus the window (x-axis). Each window’s mean value represents the mean calculated over the entire historical record for all 17,330 time series.

Natural Log

The curve of best fit displayed above is:

ln(y) = a + b * ln(x), where y represents the mean value outputted by The Bubble Index software and x represents the window.

a = -9.746393

b = 3.613444

Taking this function and rearranging the terms produces:

y = exp(a) * x ^ b, where y represents the mean value outputted by The Bubble Index software and x represents the window. (constants a and b are as above).

Exponential

To incorporate this information into the plots, the mean value for a given window will have Relative Power = 50.0 In other words, the output to the previous equation, which calculates the mean value for a given window, will be displayed on the website’s plots as 50.0

The next step will be to calculate an empirical distribution for each window.

Download the pdfs: